What Really Matters for Investment Decisions (or What Doesn't)

What Really Matters for Investment Decisions (or What Doesn't)

Making investment decisions was never easy, not only for your portfolio but also for professional investors. In the past couple of years, whenever I hear people asking questions about investments, it always boils down to a few short-term topics: inflation, interest rates, and economic activity. The underlying factors behind the performance of all these metrics in the short run are so complex that very few people can predict them. And even fewer would know what to do in that scenario (what to buy or sell and when). If forecasting short-term results is so complex and unlike to provide superior results, what really matters when investing your money? Sometimes, it is more important to understand what doesn’t matter and should be avoided.

A few years ago, when I started working in an investment platform company, my manager at that time presented me with a book by Howard Marks that simply changed the way I look at investments. For those who might not know him, Howard co-founded Oaktree Capital in 1995 and is the largest investor in distressed securities worldwide with over $170 billion under management. After reading many of Howard’s memos, I realized that as important as understanding the key value drivers of investments, it is to understand what is not relevant and is a waste of time or worse a waste of money.

What Doesn’t Matter:

The Illusion of Knowledge

Investors can become experts in a few companies or sectors, but it is unlikely to know enough about macro events to be able to understand macro expectations, anticipate the relevant events, and predict how those securities will react. Maybe you can get it right when the FED will raise interest rates, when and how much. You could also estimate the expected impact on the intrinsic value of company X. But understanding how much of this expectation is already incorporated in market prices can become tricky.

💡 Security prices are determined by events and how investors react to those events, i.e. in the short term, the ups and downs of prices are influenced far more by swings in investor psychology than by changes in companies’ long-term prospects.

Because swings in psychology matter more in the near term than changes in fundamentals, and are so hard to predict, most short-term trading is probably a waste of time and/or money.

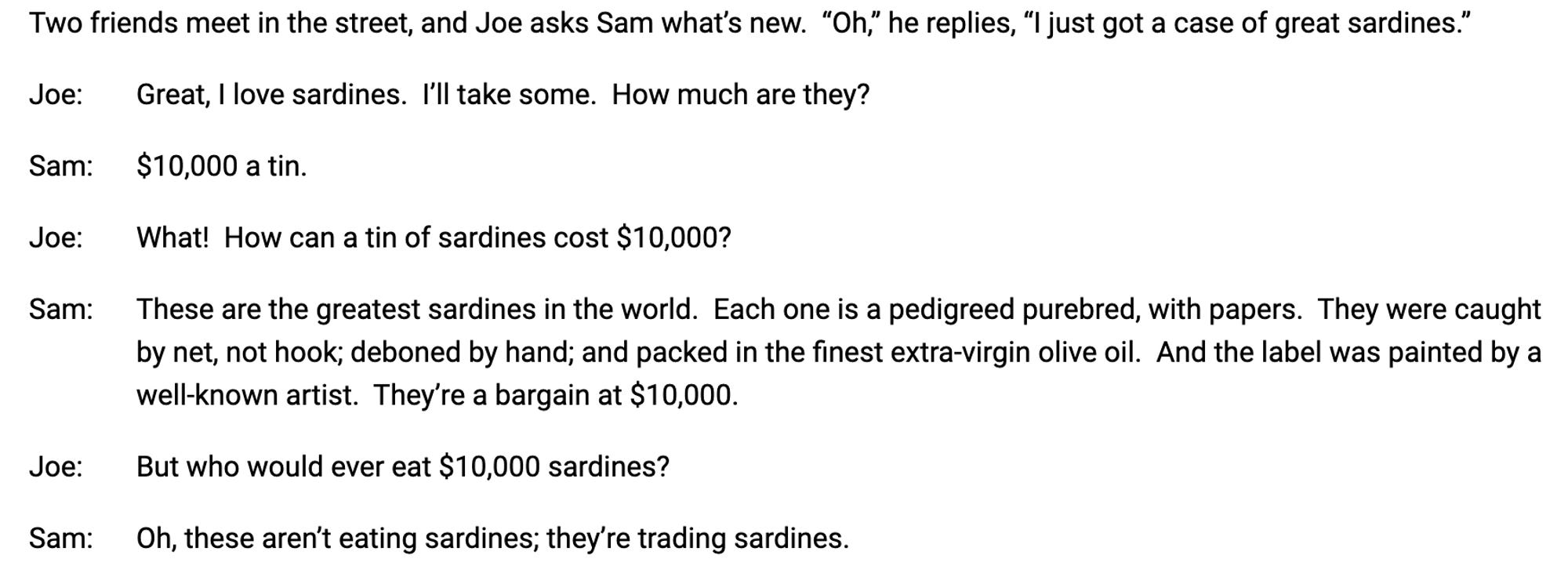

The Trading Mentality

In one of his memos, Howard shares a story his father used to tell back in the 1950s.

Great investors like Buffet and Munger would always think of buying a stock as a way to partner with the owners of the business and benefit from its profitability and growth. However, most people buy stocks to sell them at a higher price (the trading sardines), thinking they’re for trading, not for owning the business.

Of course, some people make money with trading, but I see it as a victim of The Greater Fool Theory: No matter what price I pay for a stock, there will always be someone who will buy it from me for more (even though I’m selling because I think it is at a fair value or overpriced).

💡 Each time a stock is traded, one side is wrong and one is right and if you’re betting on short-term price moves, investor psychology is more important than the company’s performance. Is it realistic to believe you’ll be right more often than the person on the other side of the trade?

Hyper-Activity

Fidelity supposedly reviewed the performance of its customers from 2003 to 2013 and found that the best investors are dead (or inactive). The best returns come from customers who either died and had their assets frozen or forgot about their assets. Although I couldn’t find the original paper, which probably means this story is fictitious, it leads to a powerful reflection.

That reflection makes me believe that investors trade too much and in fact, the study by eToro shows that the average US equity holding period is currently at 10 months vs 5 years in the 1970s. Because it’s hard to make multiple consecutive decisions correctly (getting in and out at the right time), costly to face higher transaction costs, and likely to be vulnerable to emotional swings, I believe it is better to do less trading.

Shifting the mindset from “I make money when I buy and sell something” to “ I make money (hopefully) on what I hold” should lead to superior performance. Think more, trade less.

Volatility

The concept of volatility (how much and how quickly prices move over a given span of time) is widely used as a measurement of risk. However, the recent bank crisis causing the bankruptcy of SVB and the take-over of Credit Suisse by UBS, makes me reflect on how good of a measure volatility actually is to represent risk and what are the consequences of pursuing low volatility strategies.

I acknowledge protection from volatility is a useful tool to protect us against our own emotions and cognitive biases, especially loss aversion (the pain of losing is psychologically twice as powerful as the pleasure of gaining). However, it comes at a price as favoring lower-volatility assets will lead to lower returns (all else equal). In most cases, aversion to volatility is mostly emotional and not financial. Thus, it’s crucial to understand your personal circumstances (savings, income, age, etc.) and your tolerance to losses.

Warren Buffet said to prefer a lumpy 15% return to a smooth 12% return, so investors who’d rather have the reverse (prefer a smooth 12% to a lumpy 15%) should ask themselves if the risk aversion comes from financial or emotional reasons.

I thought I was a risk-taker investor only until COVID-19 hit and I saw the effect of volatility in my behavior. I couldn’t avoid all the mistakes when I saw my stock portfolio dropping almost 60% in just a few days. That was the worst (and the best) way to understand my tolerance to volatility and how to adjust my portfolio and behaviors so I don’t make the same mistakes when it happens again (cause at some point, it will).