The M&A Window is Open - Should You Jump Through It?

The M&A Window is Open - Should You Jump Through It?

A Framework to Decide When to Build, Borrow or Buy

Current market conditions may look concerning and uncertain, inflation is high, interest rates keep rising across the globe, and the probability of an upcoming recession cannot be neglected. However, if your company has deep pockets, it could be a lifetime opportunity, given the low valuation in some sectors. According to a recent article by BCG, the current moment may be the best time in years to pursue transformative deals that radically accelerate strategy and strengthen competitive advantage. However, most acquisitions destroy value instead of creating it.

How can we better assess M&A opportunities and avoid falling into value traps?

When should we build internally, borrow from partners or buy from others?

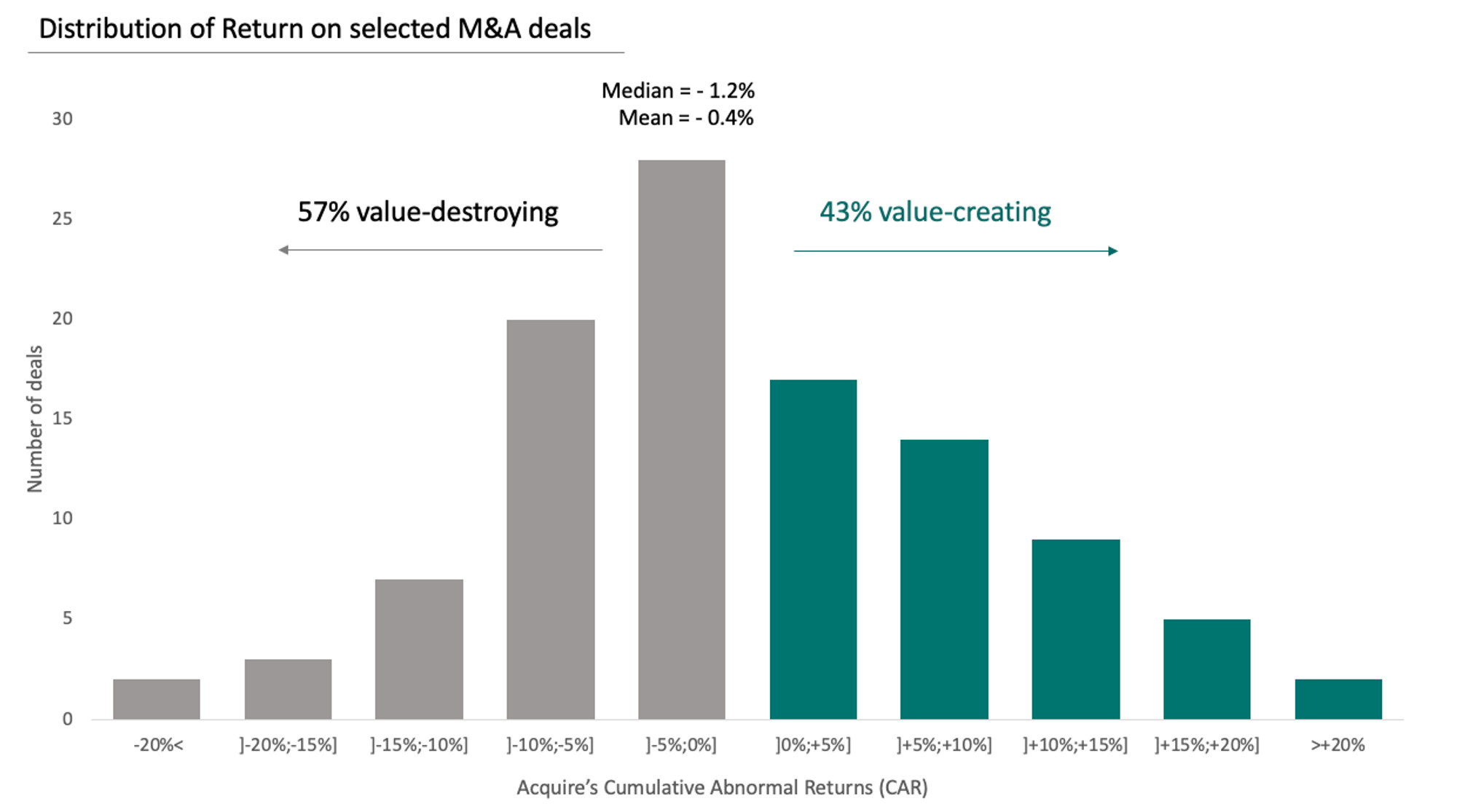

As you can see in the chart below, most M&A deals destroy value (negative returns) because integration is full of challenges, synergies can be hard to capture, and price can make good deals simply too expensive. The return on M&A deals is closely related to market cycles. The total shareholder return of acquisitions made during economic downturns was 9.6 percentage points higher than that of those made during strong-economy cycles. Take Pfizer, one of the largest pharmaceutical companies in the world, as an example. They have demonstrated opportunism and patience: during the Great Recession of 2008, they acquired Wyeth for approx. USD 68 bn, and in March 2023, they announced the acquisition of Seagen for approximately USD43 bn. My goal today is not to talk about market timing or current companies’ valuation, but I believe a structured and thoughtful decision-making process can lead to superior results.

Many firms expect acquisitions to accelerate their growth, but executives often turn to M&A for the wrong reasons, including self-interest. M&As feed managers’ egos, reputations, and dreams to build empires and show power. It also increases their compensation and masks the poor performance of the current portfolio while maintaining their attractiveness for future CEO posts. Instead, managers should focus on how potential acquisition will improve the company’s resource advantage in ways competitors could not easily match.

As you’ll notice with time, I’m a big fan of structured frameworks to tackle different problems since they help me cover many aspects of the situation, reduce cognitive biases, and lead to better decisions. I adapted this framework from the book Build, Borrow, or Buy: Solving the Growth Dilemma by Laurence Capron and Will Mitchell, and I hope you find it clear and easy to use.

Build: Are Your Internal Resources Relevant?

Internal development is usually faster and more effective but it is viable only when internal resources (knowledge, processes, and incentives) are similar to those you need to develop and superior to those of competitors. Imagine the traditional publishing firms during the transition from print media to digital. One could easily imagine that reporting, writing, and editing are the same for a web page and a printed newspaper. However, there are so many differences in the business model, customer and community interaction, technology changes, and revenue strategy that internal development can be arduous.

💡 Companies often underestimate the actual distance between their existing resources and the targeted resources. Seeing only what’s similar may lead to fixating on internal development because it doesn’t know what it doesn’t know.

Borrow: Are the Targeted Resources Tradable?

If you decided to look externally, the first option is to obtain what you need via a contract. Arm's length contracts often help companies identify, evaluate, and attain new resources and absorb them quickly. Pharmaceutical companies often license the rights to register and market other companies’ drugs in a specific market. Chemical companies out-license the rights to compounds they don’t want to develop themselves.

Although contracting is the simplest way of obtaining new resources, companies often overlook it because of trust (or lack of trust). Companies fear that they might have to give up too much revenue to a contractual partner if they don’t control commercialization or that the external party will not play fair.

💡 Important to carefully weigh potentially favorable conditions for a basic contract before going to alliances or M&A.

Borrow: Do You Need to Be Close With Your Resource Partner?

If the resources you’re trying to acquire are not tradable, you’ll need to look for Alliances, either in the form of partnerships (R&D, marketing, etc.) or joint ventures. If we go back to the example of Pharmaceutical companies, simply in-licensing the rights to a molecule can sometimes be risky because of the need to participate actively in the development process. So companies commonly use alliances, which allow partner firms to collaborate on focused projects.

However, many companies are suspicious of collaboration, and many executives overvalue control and think they will reduce their control over resources. Another concern is that alliances are usually transient relationships, so executives fear how partners could abuse them after exiting the collaboration.

💡 As a rule of thumb, Alliances are more effective when few people from each party must work together, but if joint actions require deep involvement, an acquisition will be a better option.

Buy: Can You Integrate the Target Firm?

Keep in mind that M&As are more time-consuming and expensive than even the most pessimistic scenario you could imagine (no wonder it is the last option in the framework). It is worth remembering that just 30% of M&As achieve their goals and usually involve unanticipated obstacles and expenses. A moment of low valuations like the one we are living in today will increase the chances of success, so if you value control and have analyzed and rejected the other options, then you should go for the Acquisition path, but only after you assess whether you can effectively integrate the firm's resources without damaging employee motivation at either firm.

It’s easy to underestimate the integration challenges, so you must define the scope of resource combination and resource divestiture and the integration process timeline. Even with a clear integration path, acquisition can fail if employee motivation is lacking. So it’s essential to identify the key people (how many and who they are) and retain them (align incentives and create a welcoming atmosphere).

💡 The real value of the deal comes from (i) how well the target's skills will strengthen, extend, and renew your existing resources, and (ii) how your own resources will amplify those of the target.

I hope this framework is concise and clear enough to help you make better decisions and seize opportunities, especially in the turbulent economic environment we are going through.

Great read and framework! It’s just struck me from reading this, how many companies I’ve been part of where we’ve lacked a clear structure / framework for the rationale behind a acquisition. Which seems so counterintuitive given the dent they leave on the bottom line.